As the cost of living crisis continues to bite, will this threaten to undermine the purpose-based foundations brands have built? Using data, Mark Westaby at Metricomm identifies the shift in grocery retailers’ purpose-based positioning from online media coverage.

Those of us who thought the pandemic was driving unprecedented change, the likes of which we were unlikely to see again, were clearly wrong. The world turning upside down as a result of lockdowns has been replaced by a world turning even more upside down as a result of energy prices.

Eye-watering inflation threatens an economic shock even worse than the financial crash, with costs for bailing out consumers facing crippling heating bills likely to be even greater than that of furlough during the pandemic.

Of course, all crises generate major challenges for marketing and advertising. This one, however, promises to be especially difficult given that it threatens to undermine the purpose-based foundation on which so many brands have been building their reputations. Let’s face it, given the stark choice of ‘heating or eating’, how many consumers are going to worry about the carbon footprint of their weekly shop?

Online media coverage and grocery retailers

Market research can provide some answers but given the financial worries facing so many around the cost of food, energy and just about everything else in their lives, it seems highly unlikely that many consumers will put saving the planet above their family’s welfare.

A further complicating factor is when do costs themselves become part of the purpose-based argument? Retailers have vowed to do everything they can to help cash-strapped customers, but at what point do prices on the shelves take precedence over the sustainability of ingredients in the food sitting on them? After all, what could be more purposeful for any parent than feeding their children.

In fact, we already have answers to many of these questions. Or, at any rate, evidence that can be used to address them. Metricomm’s big data analysis enables us to dive deeply into grocery retailers’ purpose-based positioning from the perspective of online media coverage, which we know from our research correlates strongly with consumer consideration and market share.

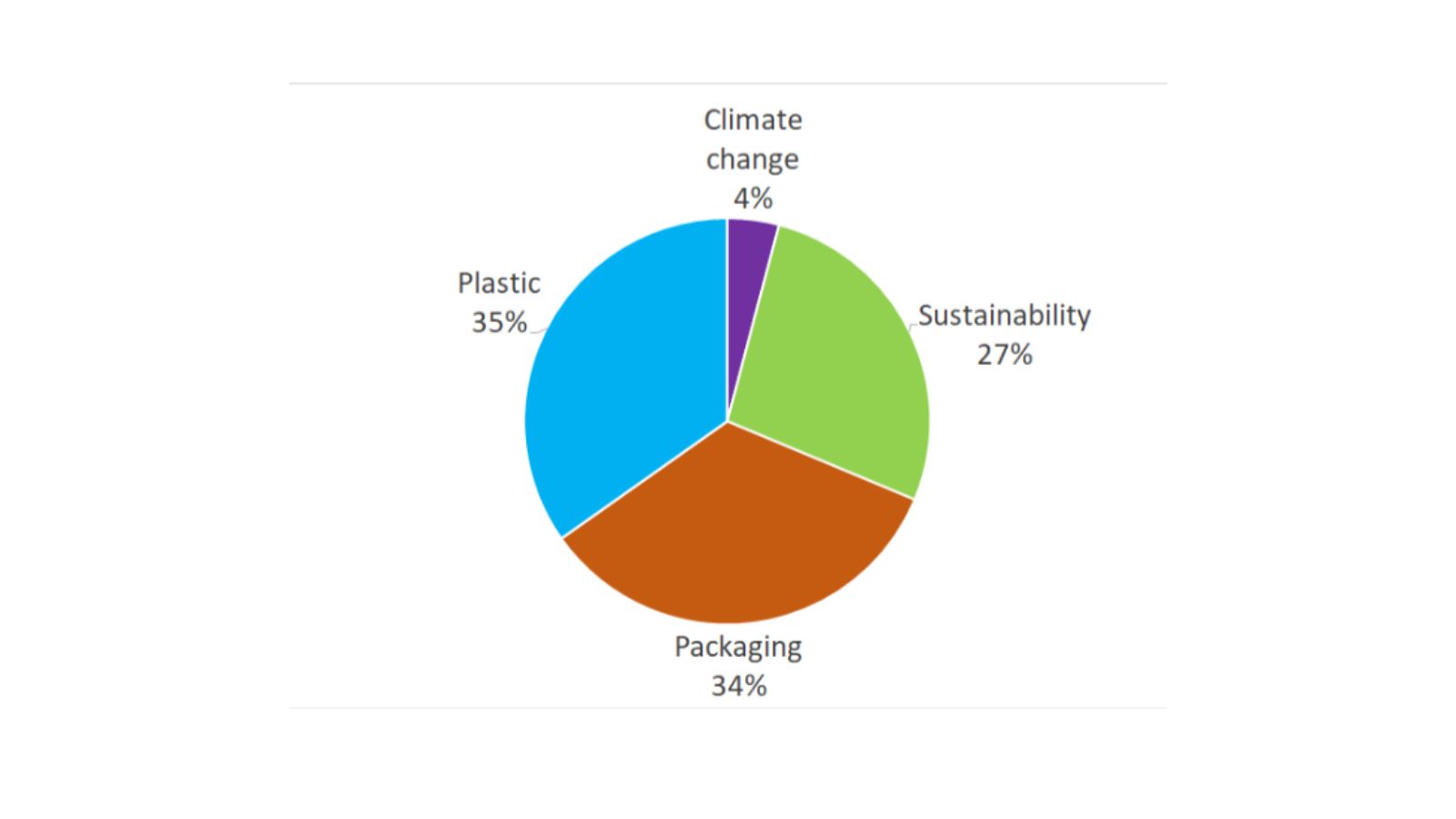

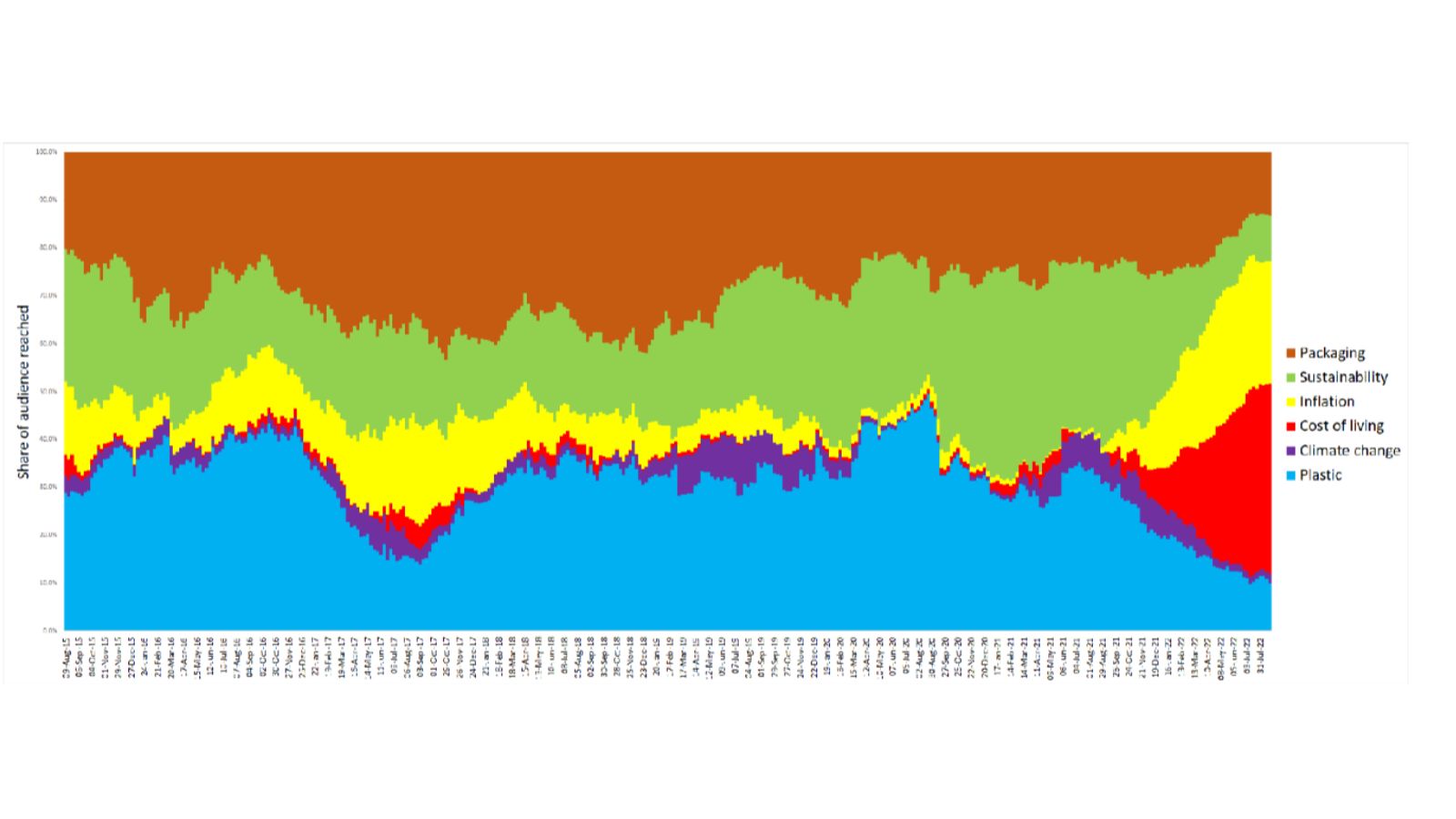

What we see when we do this is revealing. When we look at media coverage for UK supermarkets since 2015, the emphasis on purpose has been very much around packaging, sustainability and use of plastic, with climate change some way behind. Overall share of audience between each of these topics is 34%, 27%, 35% and 4%, respectively (figure 1). When we look at trends we see that the audience reached for sustainability has grown considerably since 2015, while that for packaging has reduced (figure 2).

What figure 2 also reveals, however, is the recent explosion of coverage for ‘cost of living’ and ‘inflation’, with purpose-based topics seeing dramatic falls.