With supermarket aisles on the front line of the battle for consumers’ increasingly thin resources, reputation has rarely been more important in influencing choice. Using data from its Media Audience Reputation Index, Mark Westaby, from Manchester-based Metricomm, identifies how online media coverage is closely linked to performance.

The dramatically increasing cost of living is putting retailers under renewed pressure as households struggle to meet rising prices, with energy bills, especially, taking an increasing slice out of the monthly wage packet.

Nowhere is this more acute than in the grocery sector. Supermarkets battling for market share are fighting to maintain margins, with costs predicted to rise significantly as a direct result of Russia’s invasion of Ukraine, a country that produces significant volumes of key ingredients for foodstuffs, such as grain and sunflower oil.

A key question that inevitably arises when retailers are under such pressure is who will be the winners and who will be the losers? While it would be foolish for anyone to claim they have a crystal ball, particularly during such turbulent times, there are indicators that can provide at least some basis on which the direction of market travel can be tracked.

The relationship between online media coverage and consumer interest

Metricomm’s research has revealed a strong relationship between audiences generated by online media coverage and consumer interest in the form of Google searches, which is an excellent proxy for consideration. This relationship also extends to market share and sales.

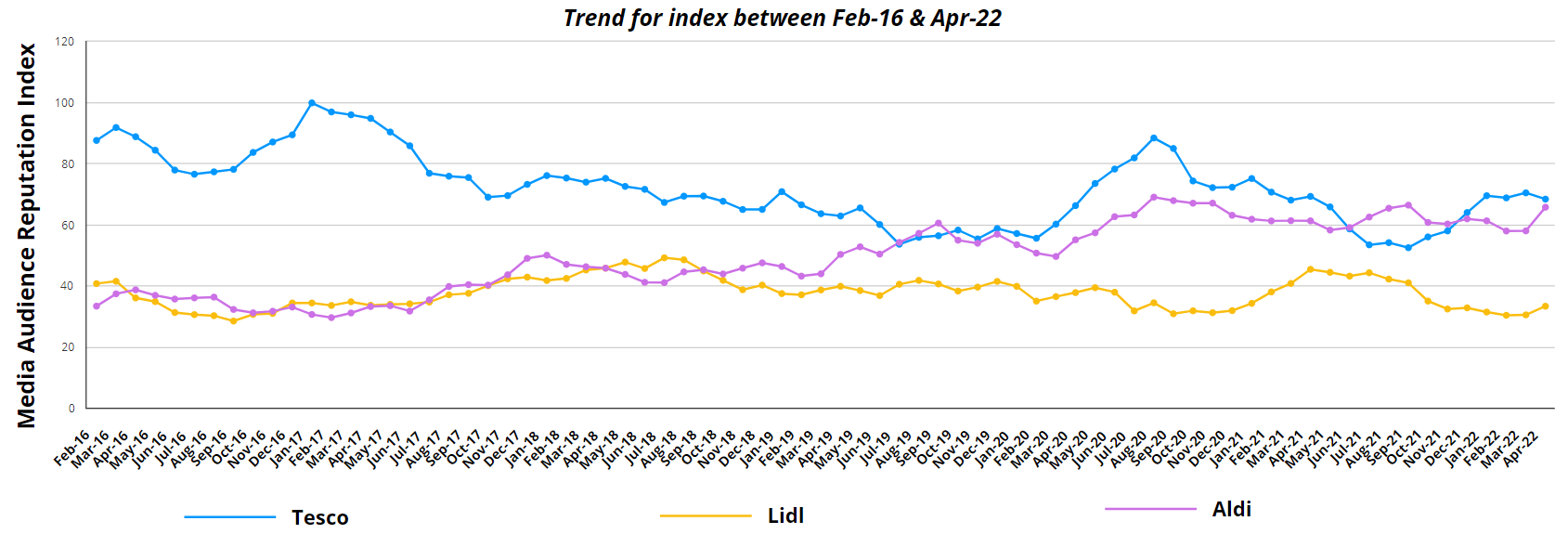

Combining trends for audiences generated by online media coverage with Google search trends provides a simple but effective indicator of how an organisation’s reputation is developing. We call this simple metric the Media Audience Reputation Index, or MARI. Just as a listed company’s share price reflects overall market sentiment, so MARI reflects the multiple factors that contribute to reputation and market share.

Above: Monthly MARI data for Aldi, Lidl and Tesco from 2016-22, reflecting the German retailers’ rapid growth and Tesco’s decline up to 2019